Financial: Is Uncle Sam Gunning For you?

Learn about RMDs BEFORE you turn 72

I was inspired to write this post by two of my good friends. I was chatting with them over the last few weeks, about their lifestyles in retirement. Both had done an exemplary job thinking about their finances. They had done their homework and worked out their budget and were living well within their means. They had done well for themselves during their working lives. One was actually a budget stickler. She tracked everything she and her husband spent and never went over budget. The other was careful to live just on the interest and dividends from her 401(k), which, again, she tracked religiously. The second wanted to pass down her entire nest egg to her children. Well… maybe… First, I have to say congratulations to them and to YOU if you are in this boat! Most of us are not. As we were discussing purpose and connections, I also I asked each of them whether they had calculated their RMDs. Both told me that they had heard of them, but they were for old people. Well… maybe…

RMD definition

According to the IRS, “Required Minimum Distributions (RMDs) generally are minimum amounts that a retirement plan account owner must withdraw annually starting with the year that he or she reaches 72 (70 ½ if you reached 70 ½ before January 1, 2020), if later, the year in which he or she retires.” (There is legislation before congress that would extend that start date for some. I’ll briefly touch on that later.) Yep. The government is not going to make you spend your nest egg, but they are going to make you take it out of your tax advantaged (retirement) accounts, so they can take the taxes. This could be an issue if you wait too long and have to take out so much that it puts you in a higher tax bracket. It could be a bigger issue if you don’t take it out and have to pay up to a 50% penalty for skipping the withdrawal.

How to calculate

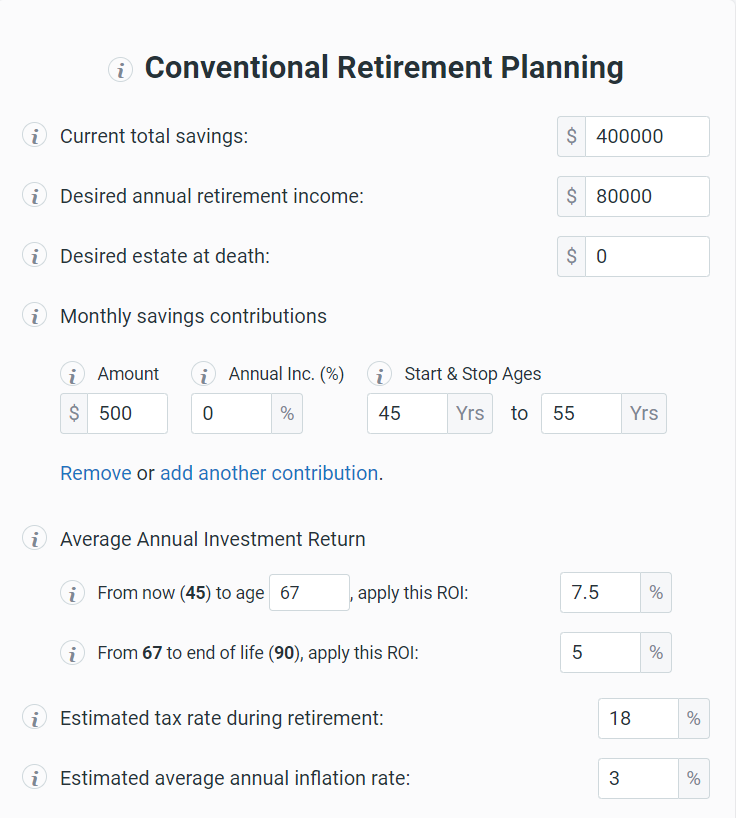

The IRS has a handy calculator for figuring out your RMDs. Unlike most government mandates, it’s actually a super simple formula. Even I get it. The hard part is figuring out how much your nest egg will be at the age of mandatory distribution, and how much you’re already going to be pulling out each month. For that, for the do-it-yourselfers, I turn to my favorite retirement calculator.

Start by adding your age, estimated age at retirement and life expectancy. Then, input your estimates for a few variables. (If you don’t know, you can Google historical averages.) REMEMBER this is going to give you an ESTIMATE, based on how good you “guess” about these variables. It’s probably going to be good enough for you to get an idea of whether you’ll have a big withdrawal that you’ll need to take, though.

Don’t forget to add your social security income stream where it says “Post retirement income streams.” There are some other variables you can add, like income from rental property or property sales, budget reductions, income from a part time job, and the like, if you want an even better picture. You’ll get something that looks like this:

You can plug your year end balance into the RMD calculator and see if it says you need to withdraw more than your pre-tax need. OR, you can talk to a professional and they can do all of this for you!

Talk to someone

If you have a good handle on your finances and you’re pretty comfortable with your picture you may be tempted to go it alone. For the day to day, that’s fine, but maybe, just for a sanity check, even you might benefit from talking to someone - especially about strategies and “gotchas” that come up all the time in tax codes and global economies. The person that wanted to pass down her 401(k)? She might talk with a CPA or CFP about gifting or other strategies that might minimize a tax bill. The one that sticks to a budget might be surprised about how much her heirs are going to enjoy HER money when she’s no longer here and she might think about ways to start enjoying it herself, now, with the help of a withdrawal strategy. Many CPAs and CFPs have an hourly rate that they charge for helping you put together these strategies. Then, they get out of your hair, if that’s what you want. (Or, if you already have an advisor, they should do it for “free,” within the fees that they already charge.) I recommend talking to someone at least once if you never have before.

New legislation

As I said, there is new legislation that is being considered that includes new rules around RMDs. It is called The Secure Act 2.0 (HR 2954 Securing a Strong Retirement) and it has passed in the House and is currently up for discussion in the Senate’s Committee on Finance. It would do several things, including increasing the mandatory distribution age. Currently, the age when an individual must begin makes distributions from retirement accounts is 72 (70 ½ if you reached 70 ½ before January 1, 2020). In 2022, that would be changed to 73. In 2029 the age would increase to 74 and in 2032 it would increase to 75. If you are not yet retired, there’s a boon for you, too, in that one of the provisions ups the “catch up” amount you can contribute. Currently, individuals who are 62, 63 and 64 can contribute up to $6,500 annually to a retirement plan. That limit would be increased to $10,000. And, my favorite thing in the bill is something that could help your grandkids. If an employee is making payments against student loans, the employer can match the amount of the student loan payment as a contribution into the employee’s 401(k). If you’re interested, you can read more about what’s included in this bill here.

Keeping up with the changes

As I said, things change in this world of investments and taxes. It’s not usually lightening speed, but over the next 30 years, you can expect some stuff. There’s a newsletter that I like that curates articles from reputable publications on what’s going on in the world of personal finance. They’re always relevant articles and topical and easy to read. (You’re not going to get the technical stuff from this newsletter. You’re going to get the practical stuff.) You can sign up for it here (scroll down to the bottom for the free sign up). And, if you don’t want to read to keep up with the changes, that’s a clue to you that you should probably call someone (preferably with a “C” in their title) at least every 3-5 years to see what you may have missed.

So don’t let RMD stand for Really Mad Dude! Calculate your RMDs, read about legislation, find a comfortable source for new information and maybe, just maybe, talk to someone who knows what they’re talking about.